After Subsea Cables Are “Lined Off,” Will Satellite Internet Be Next?

David Dong

6/22/20266 min read

On June 25, 2026, the FCC will review another regulatory item related to subsea cable security. At first glance, it seems to have nothing to do with space. But the signal it sends may say something much bigger about how the control logic of global internet infrastructure is changing.

The line under the sea is being redefined

The tightening of U.S. regulation over subsea communications cables is not a one-off policy move. It is part of a regulatory trajectory that has been developing for the past two years.

The timeline can be understood roughly as follows:

2024 The FCC launched a systematic review of national security, law-enforcement, foreign-policy, and trade-related risks within the subsea cable licensing framework.

July 17, 2025 The FCC adopted a new round of formal rules together with a Further Notice of Proposed Rulemaking, strengthening oversight of cable landing arrangements, Submarine Line Terminating Equipment (SLTE), participants linked to foreign adversaries, and ongoing disclosure and compliance obligations for existing license holders.

June 25, 2026 The FCC public meeting agenda again includes a subsea cable security item, suggesting that this regulatory logic is still being extended.

If we compress the key points from the public documents, this new phase of regulatory tightening is mainly reflected in three shifts:

extending national security review beyond the cable landing license itself to include equipment, operations, and control structures;

imposing stronger restrictions on arrangements involving “foreign adversary”-related entities, especially where those entities could access, install, own, or manage SLTE tied to U.S.-landed cable systems;

reinforcing the idea of continuous disclosure and continuous oversight, rather than one-time approval.

Based on the public text, the FCC in 2025 had already formally adopted several restrictive measures. These included stronger limits on new arrangements involving cable systems landing in a “foreign adversary country,” prohibitions on certain new sharing or leasing arrangements that would allow relevant entities to install, own, or manage SLTE in U.S.-landed systems, and annual reporting requirements for certain existing license holders.

At the same time, the FCC is still seeking further comment on whether all SLTE owners and operators should be brought into the licensing framework.

In other words, this is not simply about blocking a particular device. It is about treating subsea cables as a category of critical infrastructure that must be governed simultaneously at the level of physical assets, control rights, and supply chains.

Subsea cables are not peripheral infrastructure

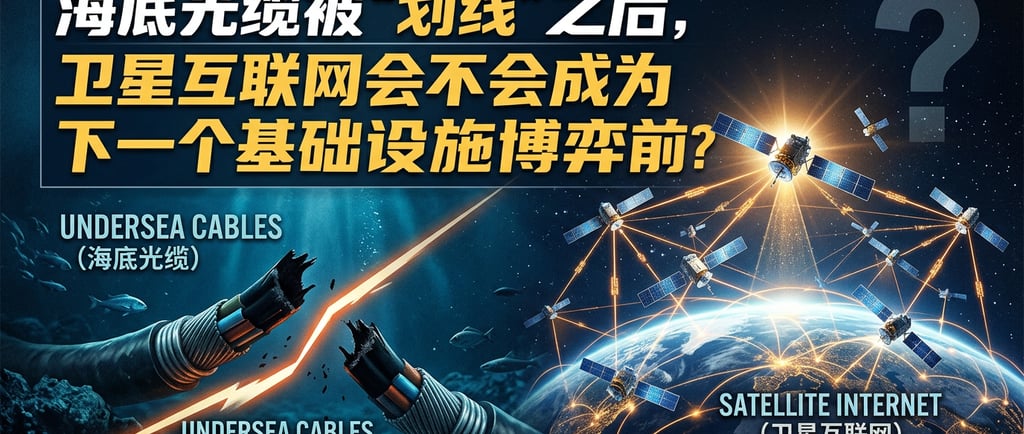

Subsea cables are not a marginal part of the internet. They are one of its foundational layers.

A common industry view is that the overwhelming majority of intercontinental data traffic moves through subsea cables. Many reports place that figure above 95%, and it is also often described as being close to 99%. Whatever the exact number, the conclusion is clear: cross-border payments, video conferencing, cloud service calls, cross-border e-commerce, and content delivery all depend on physical links lying on the seabed.

That is why subsea cables have never been merely a telecom engineering issue. They are also:

a national security issue,

a supply-chain issue,

an industrial control issue,

and a geopolitical issue.

And that is exactly why the latest FCC moves matter.

The United States is no longer approaching subsea cables only through the traditional lens of communications licensing. It is moving toward a broader framework of infrastructure control.

If the sea becomes constrained, can the sky provide the alternative?

Against this backdrop, a natural question emerges:

If the physical layer of subsea cables is increasingly being “lined off,” could satellite internet become an alternative path around those constraints?

From a technical standpoint, this is not a strange question.

Low-earth-orbit constellations do offer a different model for cross-regional connectivity. Systems such as Starlink have already developed into global-scale networks. According to SpaceX’s 2026 public disclosure, as of March 31, 2026, Starlink had approximately 10.3 million subscribers across 164 countries, territories, and markets.

Compared with subsea cables, one important attraction of LEO satellite systems is that, at least in principle, they can partially reduce dependence on a single traditional subsea route for transoceanic connectivity.

But that does not mean satellite internet is naturally free from infrastructure control problems.

On the contrary, the logic of control may simply have changed carriers rather than disappeared.

Satellite internet has its own physical control points

If the key control points in the subsea cable world can be summarized as landing stations + terminating equipment + licensing systems, then satellite internet has its own equivalent structure. At least three areas deserve close attention.

1. Spectrum and orbital resources

Satellite spectrum and orbital resources are coordinated under the ITU framework. Publicly available materials show that the core logic of the ITU system is to prevent harmful interference, promote coordination and registration, and use milestone mechanisms to prevent long-term warehousing of resources.

In practice, the framework has a clear “first to file, first to coordinate” character. But it is not a simple, unconditional first-come-first-served system.

What does that mean?

It means that for latecomers, the key question is not simply whether they can build satellites. It is whether they can:

file in time and complete coordination;

meet deployment milestones;

secure sufficiently usable conditions in increasingly crowded bands and orbital environments.

As LEO constellations expand rapidly, these issues are no longer abstract. They are becoming real barriers to entry.

2. Ground gateway stations and landing permissions

Many people imagine satellite internet as a network detached from terrestrial infrastructure. That is not quite accurate.

Even if inter-satellite laser links improve transmission capacity between satellites, data still ultimately needs to come down at certain nodes and connect into terrestrial networks, cloud infrastructure, and local backbone systems. In that sense, satellite networks do not eliminate “landing stations.” They relocate them from the coastline to ground gateways and access nodes.

And once you see it this way, the core questions remain the same:

Where are those nodes built? Who operates them? Which jurisdiction governs them? Can they obtain the necessary approvals?

At their core, these are still questions of control.

From this perspective, the FCC’s governance logic for subsea cables could very well become a regulatory template for tighter governance of satellite ground infrastructure in the future. The legal frameworks are not identical, but the underlying logic is structurally similar.

3. Satellite manufacturing and critical component supply chains

When subsea cable systems get constrained, it is often not only because of licensing. It is also because key components, equipment, and technical processes are concentrated in a small number of supply-chain nodes.

The satellite sector is no different.

Radiation-hardened chips, inter-satellite laser communication terminals, certain high-reliability components, attitude-control subsystems, and sensing-related parts can all become new points of dependency.

That means even if a country has constellation plans, launch capability, and market demand, it may still be constrained in real competition if it has not built enough resilience into the supply chain for critical components.

The deeper implication

At a minimum, the regulatory tightening around subsea cables tells us one thing:

Competition over global network infrastructure is becoming less about whose technology is more advanced and more about who gets inside the rules, who controls the nodes, and who owns the supply chains.

Under that logic, satellite internet may indeed become a kind of workaround in some scenarios.

But it may also become the next infrastructure layer where access boundaries are explicitly defined and enforced.

So the real question is probably not just whether satellites can replace subsea cables.

It is this:

As subsea infrastructure becomes more politicized and more institutionalized,

will space infrastructure gradually enter a similar control framework?

Will spectrum-orbit coordination, ground stations, and supply chains become the new “landing stations” and “equipment reviews” of the satellite internet era?

These issues have not fully materialized yet.

But they are already serious enough that they should not be left for later.

What is the real challenge for China’s satellite internet sector?

If the current shift in subsea cable governance is an early signal, then the challenge facing China’s satellite internet sector is not merely one of catching up in isolated technologies.

The more difficult questions are systemic:

Is it sufficiently prepared for long-term spectrum-orbit coordination and rule-based competition?

Does it have a durable plan for overseas ground nodes and external landing architecture?

Does it have enough native redundancy in critical components and core supply chains?

Is it ready for a future shaped by white lists, trusted vendor regimes, and licensing reviews?

This is no longer only an engineering issue. It is not even only a commercial issue.

It is a geostrategic issue at the level of infrastructure.

Closing

It may still be too early to draw definitive conclusions.

But at the very least, this is no longer a question that can be postponed until after the next round of rules is already in place.

LU FRONTIER STRATEGIES

© 2026 LU Frontier Strategies. All rights reserved.